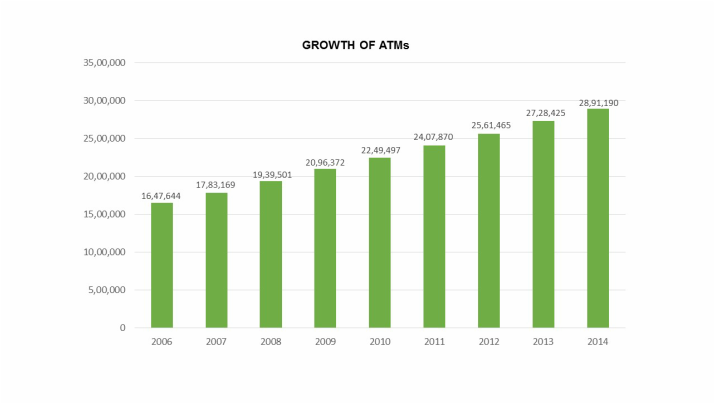

Ayan Prabhakar Baruah, B-Tech GPT 2nd Year

Unlike the Brown Label ATMs which have the parent bank’s logo, White Label ATMs (WLAs) are machines deployed by non-banking entities which charge banks a fee whenever account holders transact. In terms of the older rules and regulations, only banks were permitted by the RBI to set up ATMs as extended delivery channels. Banks have played a major role in modifying behavioral strategies in personal banking domain. ATMs have been leveraged to deliver a wide range of banking services to customers. Although there has been nearly 23-25 % year-on-year growth in the no. of ATMs, they have penetrated Tier I & Tier II centres predominantly. Feeling the need to expand reach of ATMs to Tier III to VI centres, RBI decided in 2012 to permit Non-banking entities to operate ATMs in India.

Readers interested to know more about the guidelines issued by the RBI may check the RBI website for the full length document. As per the RBI Guidelines, minimum net worth necessary for non-banking entities to set up ATM services should be 100 crores.

Since 2013, the RBI has licensed 7 players — BTI Payments, Tata Communications Payment Solutions (TCPS), Prizm Payment, Muthoot Finance, Srei Infrastructure, RiddiSiddhi Bullions and Vakrangee Limited. 3 more companies are expected to join. RBI norms require that these companies set up ATMs in mostly towns and villages which banks have failed to cover. WLA operators get interchange fee of ₹15 per transaction from the bank whose customer uses the ATM. The government’s move to open bank accounts for all under the PMJDY might give a medium term boost to usage and make WLAs viable in rural areas, the long term viability is challenging due to low volume environment in many areas, and some villages have population only in thousands. Suggestions have been made to reduce operating costs:

1. Remove restrictions that allow only sponsor bank to load the cash

2. Allow WLAs to recycle cash received for deposit

BTI Payments is reducing costs by deploying ATMs in kirana stores and also considering the idea of mini ATMs of the size of coffee machines.

Despite the innovative ideas and the no frills approach, they are struggling with long term viability and operators are seeking increase of interchange charge from ₹15 to ₹18. In December 2014, the RBI allowed the use of international credit and debit cards in WLAs. Although RBI has welcomed the concept of WLAs, it still falls short of making them viable and operators are dependent on cost cutting measures for sustainability.

Unlike the Brown Label ATMs which have the parent bank’s logo, White Label ATMs (WLAs) are machines deployed by non-banking entities which charge banks a fee whenever account holders transact. In terms of the older rules and regulations, only banks were permitted by the RBI to set up ATMs as extended delivery channels. Banks have played a major role in modifying behavioral strategies in personal banking domain. ATMs have been leveraged to deliver a wide range of banking services to customers. Although there has been nearly 23-25 % year-on-year growth in the no. of ATMs, they have penetrated Tier I & Tier II centres predominantly. Feeling the need to expand reach of ATMs to Tier III to VI centres, RBI decided in 2012 to permit Non-banking entities to operate ATMs in India.

Readers interested to know more about the guidelines issued by the RBI may check the RBI website for the full length document. As per the RBI Guidelines, minimum net worth necessary for non-banking entities to set up ATM services should be 100 crores.

Since 2013, the RBI has licensed 7 players — BTI Payments, Tata Communications Payment Solutions (TCPS), Prizm Payment, Muthoot Finance, Srei Infrastructure, RiddiSiddhi Bullions and Vakrangee Limited. 3 more companies are expected to join. RBI norms require that these companies set up ATMs in mostly towns and villages which banks have failed to cover. WLA operators get interchange fee of ₹15 per transaction from the bank whose customer uses the ATM. The government’s move to open bank accounts for all under the PMJDY might give a medium term boost to usage and make WLAs viable in rural areas, the long term viability is challenging due to low volume environment in many areas, and some villages have population only in thousands. Suggestions have been made to reduce operating costs:

1. Remove restrictions that allow only sponsor bank to load the cash

2. Allow WLAs to recycle cash received for deposit

BTI Payments is reducing costs by deploying ATMs in kirana stores and also considering the idea of mini ATMs of the size of coffee machines.

Despite the innovative ideas and the no frills approach, they are struggling with long term viability and operators are seeking increase of interchange charge from ₹15 to ₹18. In December 2014, the RBI allowed the use of international credit and debit cards in WLAs. Although RBI has welcomed the concept of WLAs, it still falls short of making them viable and operators are dependent on cost cutting measures for sustainability.